I hear you already, “If I’m broke, is there any point in reading about finances?” The answer is yes! If you are really “broke, broke,” like $0 and in debt, then of course, it’s not rocket science to know that the best thing to do is figure out how to generate some extra income: tutor on the side, add a side hustle, get a campus job, pay off any debt, etc. But what if you are a student or someone who does make ends meet and you have some extra earned money sitting in the bank or in your desk drawer?

Aside from keeping a small emergency fund, here is the one thing I recommend: contribute to a RothIRA account on Vanguard!!! It’s designed to help people below certain income limits invest money for growth. I grew up in humble beginnings, and I wish I knew this when I was younger.

Earned Income + What is a Roth IRA

If you have earned income (from babysitting, tutoring, etc.) at any age that you are able to show on taxes, you can contribute to a RothIRA. So, why is this account so special? Well, unlike keeping your money in the bank and just letting it sit there, if you put your money in a RothIRA account, the money will grow with the market (5-6% returns), and the best part is that it grows tax free, so you don’t pay taxes on it when you take it out. So, it’s superior to saving money in the bank, or investing traditionally where you have to pay capital gains taxes. Because this account is so amazing, there is a limit on how much you can contribute and who can contribute (income limits). Although, for high-earners above the income limit, there is a Backdoor RothIRA option to be discussed later.

Is A Roth IRA Risky?

So, the usual concerns are, “Is my money safe in this account? How can I trust it? What if the market crashes? I don’t know, the investing stuff sounds risky.” Everyone has these thoughts at first. Historically since the beginning of the stock market, the market performance is that it always recovers and it always goes up. No one can time the market, and by the time you even take your money out and transfer it, or put more money in, the market may have already gone back up or down and you lose out on the earnings. So the best thing to do is to think long-term, invest in index funds (VTSAX etc.), "set and forget" and let the funds do their thing. When you are closer to retirement, you can change your fund option from high-risk (more growth) to low-risk (less growth) because you will soon pull your money out, and now you don’t want to risk losing with any major changes to the market (which again, no one can predict or time).

2020 Roth IRA Limits

- $6,000 if you're under age 50

- $7,000 if you're age 50 or older

- And you have to have earned less than 124K if you are single and less than 196K if you are married.

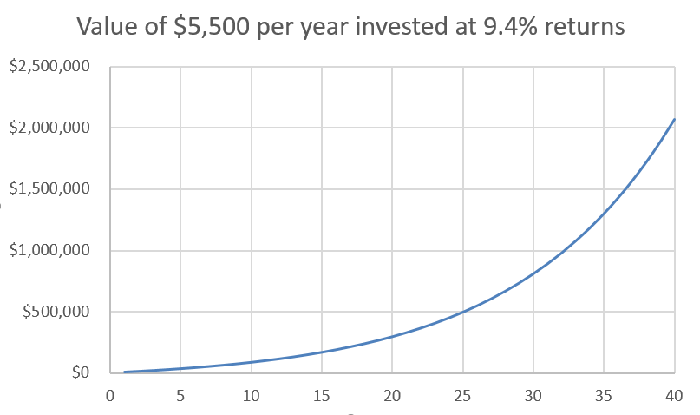

Get your friends in on this and talk about it because I promise it will build stronger friendships! Take a look at this simple graph which I hope is eye-opening.

If you take a look, the graphs shows that if you invest $5,500 a year for 40 years in a RothIRA, your account will grow to over 2M dollars! How amazing is compound interest?!

What If You Are A Low Income College Student

One caveat that I haven’t seen discussed in many places is what if you are a low income college student, such as an EOF student, and FAFSA or your school wants you to list any investment accounts? This may be a conflict of interest with your aid, and it varies from school to school depending on what they ask in their financial aid application. If you are unsure, and you don’t want to risk losing financial aid, you may want to wait to start this type of investing until after you graduate.

Learn MORE About Finances Than Wealthy People

I like this quote that Mellody Hobson, President and co-CEO of the $13 billion money management firm Ariel Investments has said (I find her to be a role model, and she grew up in humble beginnings): “I was desperate to understand money. Not to make it, but to understand it. I wanted to know how it worked, and I wanted to know so that I would have enough and would be able to make good financial decisions." I feel the same way, I think if you are “broke” or have little money, you should learn about finances MORE than other (wealthy) people because you want to figure out how this finance world works and how to earn more and generate wealth.